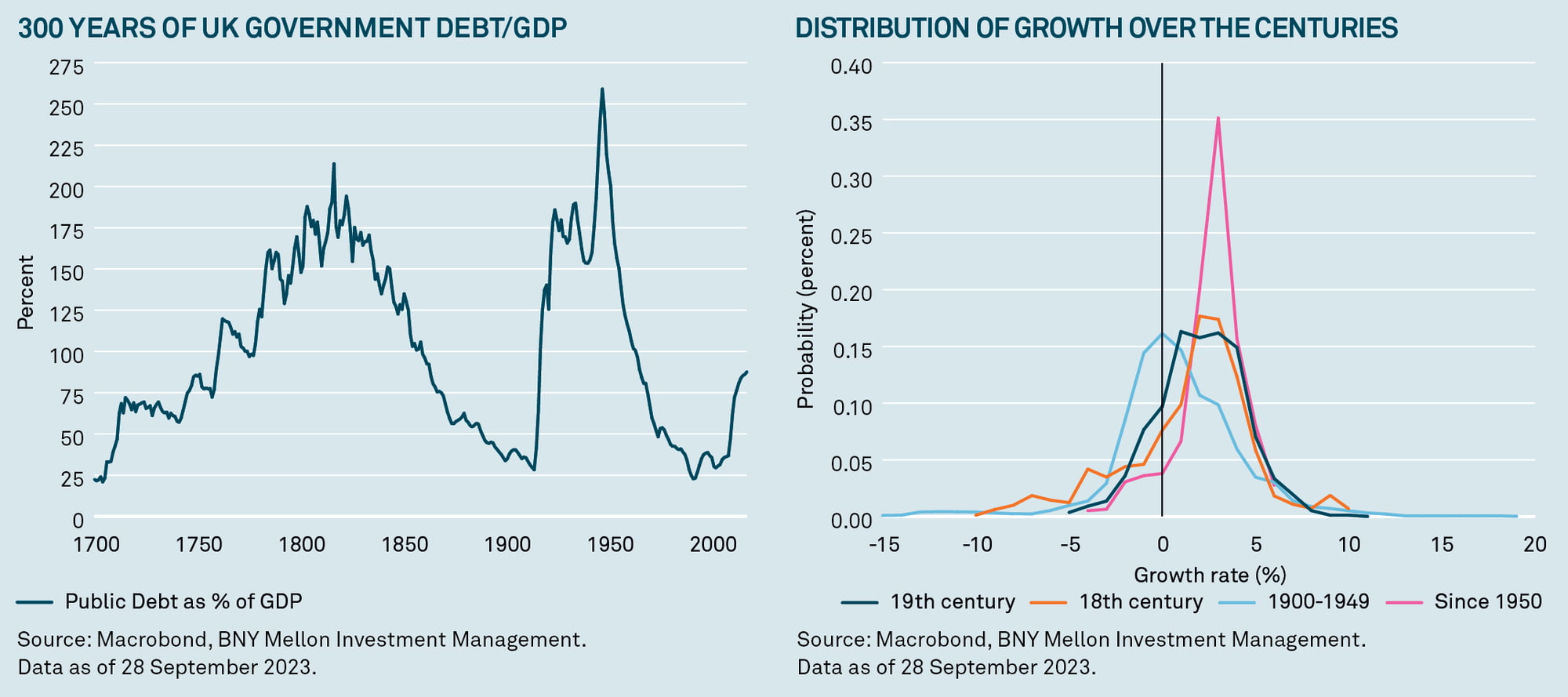

But as evidenced by the UK’s gilt crisis in October 2022, debt sustainability concerns are not just reserved for emerging markets, Dhar points out.

That’s just one view. There are those that believe the opposite, what Dhar calls the “financial repression” argument. If government debt is high, the required actions necessary to address it may be too painful so they take actions to bring the debt-to-GDP ratio down instead.

“This means holding the (nominal) yield on government debt below the (nominal) growth rate of the economy for some time. Ultimately, this amounts to ‘inflating away’ the public debt and is an implicit tax on bondholders.”

There is also a third argument – that there is no relationship between government debt levels and rates.

Dhar says it’s hard to even take a guess which of the three possibilities might be right. Government debt remains an influence to watch but right now has the least clarity. He adds: “The safe asset shortage is likely to persist and the incentive to financially repress will be high. So, which of these three possibilities is likely to best explain the next few next decades? The truth is we don’t know, and our inclination is to assume they will roughly offset each other.”